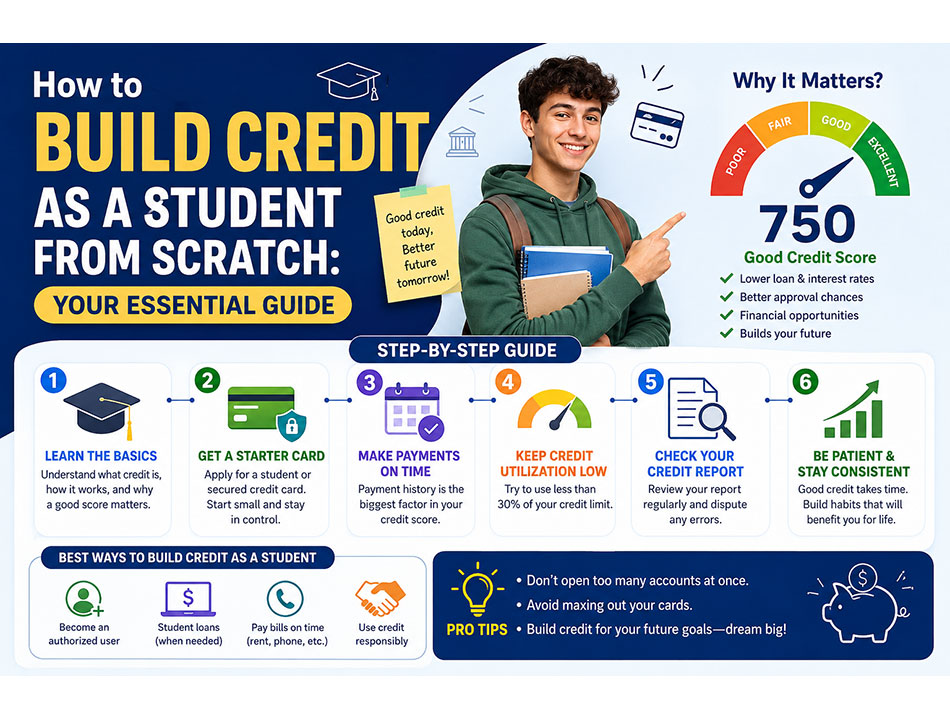

Student credit cards have become a crucial tool to help students stay focused on their studies when they run short of money. Running out of monthly allowance is a common experience for young students who stay in hostels or away from home for studies. Even students in big cities who stay with their families also often face a similar experience when they run out of pocket money.

There is a common misconception among students that credit cards are for working people. There are also concerns among students about getting trapped in high-interest repayment cycles. If you are a student, these concerns are quite understandable. Fortunately, there are credit cards for students that address almost all of these concerns. These cards, apart from helping you with your day-to-day financial troubles, can also help you to build a solid credit score that, in the future, will help you to secure other loan products from banks and financial institutions.

Here in this guide, we are going to explore every major student credit card in India, along with their fees, rewards, and respective pros and cons of each card.

Why Student Credit Cards Exist and Who They Cater To?

The vast majority of student credit cards in India are secured ones. Secured credit cards typically link the credit limit to a Fixed Deposit (FD) that the applicant or the guardian of the applicant has with the bank. While most FDs earn interest of around 7%, the student credit card issued linked with the credit card comes with an 80 to 100% spending limit of that deposit amount. These secured student credit cards or credit cards against FDs do not need any income proof or credit history to issue the cards. Any 18+ student with an FD in his name is eligible for these cards.

Two government-backed student credit card schemes serve as low-interest education loan instruments for students. We have the Bihar Student Credit Card Scheme (BSCC) and the West Bengal Student Credit Card Scheme (WBSCC). Unlike the regular plastic credit cards, these are a sort of education loan product aimed at students. Students who do not have a substantial amount lying in FDs can rely on them. The Bihar Student Credit Card Scheme (BSCC), for instance, offers students loans up to ₹4 lakh at just 4% interest for males and 1% interest for transgender and females.

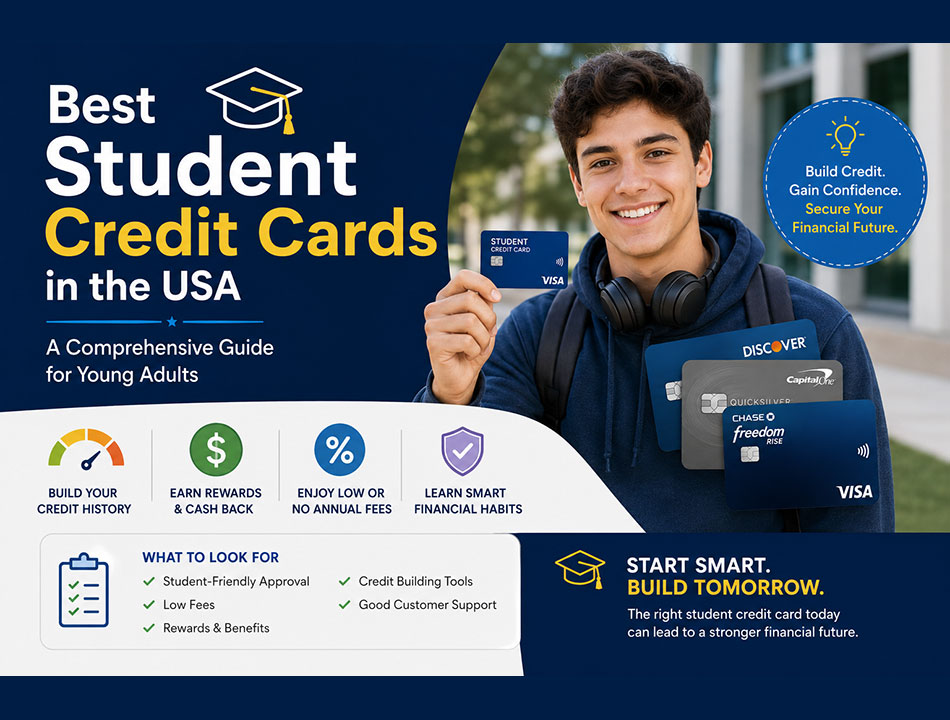

Every Major Student Credit Card in India: Everything You Need to Know

1. IDFC FIRST WOW Credit Card

DFC FIRST WOW is by far one of the best student credit cards, in terms of ease of use and low-bar conditions.

Fees & Charges:

- Joining Fee: Zero

- Annual Fee: Zero fee for lifetime

- Minimum FD Required: Only INR 2,000 is required as FD, which is the lowest compared to any other cards in the market.

- Interest Rate: Monthly interest rate of 3.99%, which amounts to 47.88% per year.

- Forex Markup Fee: Zero

Cashback & Rewards:

- The card offers 4X reward points on all spending instances, whether online, offline, or international transactions. The actual reward is INR 1 for every INR 50 spent in any transaction.

- 1X reward points on transactions for utilities such as electricity and gas, insurance premiums, FASTag recharges, and railway tickets. The actual reward is INR 1 for every INR 200 spent.

- The linked fixed deposit earns 7.5% yearly interest.

- For the first 48 days after the issuance of the card, students can avail the benefit of withdrawing money from any ATM without paying any interest.

Pros:

- Students can have a credit card without paying any fees.

- The credit card requires only a deposit of INR 2000, which is the lowest in the industry.

- The card comes with no constraints in relation to foreign currencies and this makes it very useful for students studying abroad or traveling

- Availability of 100% of the FD value as the credit limit and cash withdrawal limit.

- The application process is fully digital, and no paperwork is required.

- For eligibility, no credit history or income proof is required.

Cons:

- The rewards for spending on utility bills and insurance premiums are very low, as it is capped at 1X.

- The credit card doesn’t offer airport lounge access for the regular variant. The same is available with the premium WOW Black variant.

- The cash advance fee of ₹199 for every transaction becomes a pain point for students who use ATMs frequently.

2. Kotak 811 #DreamDifferent Credit Card

This is another student credit card that has become immensely popular in recent times among students who are digitally active. The 811 account related to the card functions through an app. Like many other secure credit cards, Kotak 811 student credit cards also require having an FD.

Fees & Charges:

- Joining Fee:

- Annual Fee: The annual fee is free for the first year, and from the second year, the fee is INR 500 per year. The annual fee for any year is waived if the previous year's spending value is INR 50,000 or above.

- Minimum FD Required: A minimum of INR 15,000 FD is required to avail the card.

- Interest Rate: As for interest rates, standard Kotak Mahindra Bank interest rates apply.

- Fuel Surcharge Waiver: From June 2025, the cardholders get a waiver of 1% on fuel purchases amounting to between INR 500 and INR 4,000, and the maximum waiver amount is capped at INR 3,500 for every year.

Cashback & Rewards:

- The cardholders get 2 reward points for every 100 rupees spent online.

- For all other transactions except online spending, you get 1 reward point for every 100 rupees spent.

- After having the card. Within the first 45 days, the users get 500 bonus reward points as a welcome benefit for just INR 5,000 of spending.

- If you have spent more than or equal to INR 75000 in a calendar year, you will get either an INR 750 cashback or 4 PVR movie tickets, as per your preference.

- The credit limit for the card stands at 90% of the FD value

Pros:

- This credit card is completely app-based, ensuring a seamless digital-first experience.

- The welcome bonus is quite within the range of average student credit card users.

- Milestone benefits, such as movie tickets or cashback, are great for students.

- The waiver of the railway surcharge for all IRCTC bookings made using the card is also a great boon for students.

Cons:

- You need to pay a ₹500 annual fee after the first year if you could not spend as much as INR 50,000 in the previous year.

- Since June 2025, many reward points for the card have been excluded such as education, wallet loading, fuel, rent, government, insurance, and spending on online games.

- Compared to the most competitive cards in the market, the reward points are substantially lower.

3. SBI Student Plus Advantage Credit Card

The SBI student credit card is one of the oldest and most widely available options — partly because SBI has branches in literally every district of India. It's issued either against an SBI education loan or an FD.

Fees & Charges:

- Joining Fee:

- Annual Fee: There is no annual fee for the first year, but you need to pay INR 500 every year from the second year. The annual fee is automatically waived for the next year if your spending value goes over INR 35,000.

- Interest Rate: The interest rate is 2.25% per month, which amounts to 27% per annum.

- Foreign Transaction Fee: The interest rate for foreign transactions is 3.5%.

- Cash Withdrawal Limit: You can withdraw up to 80% of your credit limit as cash.

- Interest-Free Period: The interest-free period for the spending is 20 to 50 days.

- Late Payment Fees: The late payment fee for all dues between INR 200 to INR 10,000 is ₹100, and beyond that, the fee is INR 750.

- Reward Redemption Fee: To redeem the rewards, there is a fee of INR 99.

Cashback & Rewards:

- The cardholders get 1 reward point for every 100 rupees spent, and they can redeem the points against any outstanding bill.

- You get 10X reward points for all your spending in departmental stores and for your spending on groceries.

- You get a 2.5% surcharge waiver for buying fuel at any petrol pump.

- FlexiPay option: This option allows users to convert any transaction beyond ₹2,500 into easy monthly installments.

- This card is widely accepted, covering 24+ million outlets worldwide and 3,25,000+ outlets in India.

- The card also supports booking railway tickets online.

Pros:

- The card can be availed by the borrowers of SBI education loan, without having any FD.

- The card is widely accepted with both Visa and Mastercard support.

- Fuel waiver is practical and straightforward

- The card offers the highest reward points for spending on groceries and shopping in departmental stores.

Cons:

- With a 3.5% foreign transaction fee, it is one of the most expensive student credit cards when it comes to overseas use.

- The fee of INR 99 for redeeming rewards is a meaningless burden as users need to pay for using their own reward points.

- The interest rate of 27% per annum is also very high for anyone who fails to repay the credit in time.

4. ICICI Bank Coral Contactless Credit Card

Though it is not referred to as a credit card for students only, students can find it really useful, particularly because of the extensive rewards and insurance options backed by the FD.

Fees & Charges:

- Joining Fee: The joining fee for the card is INR 500 + GST.

- Annual Fee: The annual fee is INR 500 plus GST, but it is waived for users who spent INR 1,50,000 in the previous year.

- Minimum FD Required: Only 20,000 is required as the fixed deposit for the card.

- Interest Rate: The interest rate is only 3.50% per month.

- Cash Advance Charges: Standard ICICI rates are applicable for cash advances.

Cashback & Rewards:

- The users get 2 reward points for every 100 rupees spent on all purchases.

- The reward point is only 1 for every 100 rupees spent on utilities and insurance premiums.

- The users can easily redeem the reward points across a multitude of partner outlets and facilities.

- Users can also get a 1% waiver on the fuel surcharge across all HPCL petrol pumps.

- Users can avail up to 15% discounts when dining at more than 2,500 selected restaurants across India.

- The card users can also avail 25% discount on movie tickets booked through the BookMyShow platform.

Pros:

- Users of this card get much higher reward rates compared to other student-specific cards in the market.

- It is a great card for students who prefer eating out frequently, as the card offers great discounts on restaurant dining.

- You also get a seamless digital experience thanks to ICICI's mobile app and the bank's widespread network.

Cons:

- The card has a joining fee, unlike most other student credit cards.

- The transaction amount required to get the waiver for the second year's annual fee is quite high compared to most other cards.

- The required FD of INR 20,000 is also higher compared to several other student credit cards.

5. Kotak811 Super Money Credit Card

This is another secured card from Kotak Mahindra Bank and Super. Money, that can help students who transact a lot across digital platforms.

Fees & Charges:

- Joining Fee: Zero

- Annual Fee: There is no annual fee for the entire lifetime.

- Minimum FD Required: The required FD amount is only INR 1,000.

- Interest on FD: The interest rate on FD is 6%.

Cashback & Rewards:

- The card users get 5% cashback on Myntra, 3% cashback on Cleartrip, and 2% cashback on Flipkart.

- Across other online platforms and apps, they also get a 1% cashback on all purchases.

- The users can only redeem the Cashback amount through the Super Money app.

Pros:

- There is no joining or annual fee at all.

- The required FD of INR 1,000 is the lowest compared to all other student credit cards.

- The users get a lot of cashback options across major ecommerce platforms.

- The 1% cashback against UPI transactions is a unique advantage for the card users.

Cons:

- Since the redemption of rewards or the cashback option is locked to only the Super Money app, it is detrimental to the user’s flexibility.

- The card has very limited acceptance, and users need to opt for only the partner brands to get rewards.

Final Word

Since every card has its own share of pros and cons, Wows and pain points, naming the best student credit card in India is practically impossible. Several factors play a role, including the required FD amount, your spending choices and frequency, and your priority for credit score building or reward points. Based on your transaction patterns, priorities, and FD capacity, you can easily opt for any of the above five options.

Author

Related News