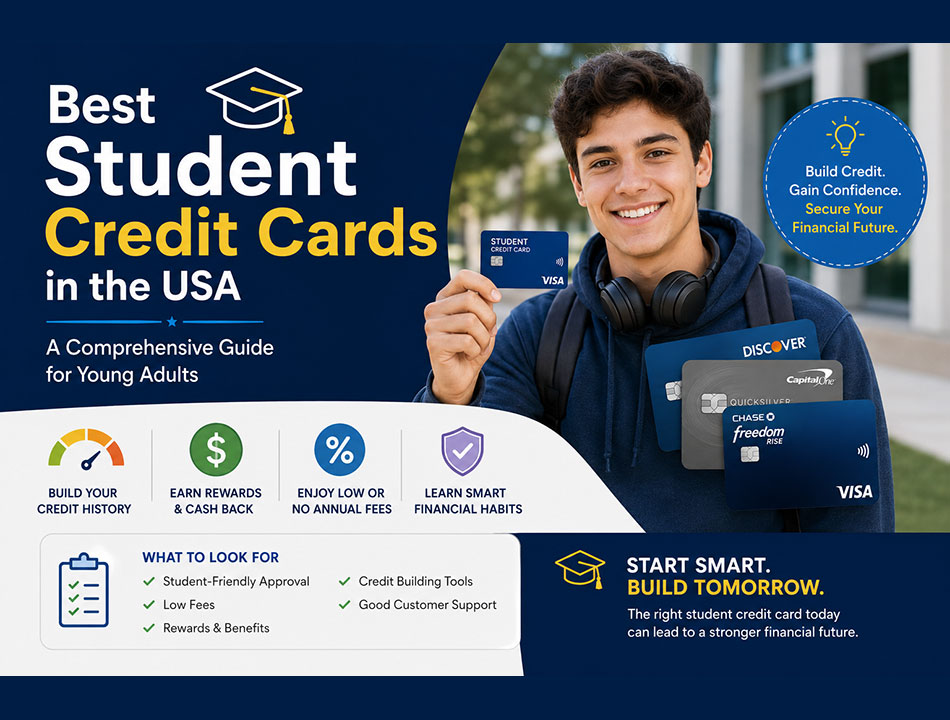

Choosing your first student credit card? Discover the 8 most important factors that every US college student digs deeper into before applying.

Do you know that the student credit card you start using in your college days can actually play a role in shaping your financial life for the years to come? No, you are neither going to use it forever nor is it going to land in your account a huge sum of cash as a reward. This is principally because the credit score you build in your college days can help you get a car loan or a home loan in the near future. Even instantly after following your graduation, if you are going abroad to study, your credit score is likely to help you get education loans.

But if you are picking your credit card for just a sign-up bonus or a prize like a free pizza, you are getting it all wrong. You should take the decision seriously and consider critical factors that matter for shaping your financial journey. While choosing a student credit card for college students in the US, consider the following factors.

1. Annual Fee: The First & Foremost Consideration

It’s the easiest consideration since student credit cards with no annual fee are still common. So, you can strike off any card that is charging an annual fee, unless it is heavily loaded with other perks and benefits. Most of the leading student credit card options like the Discover it® Student Cash Back, the Capital One Quicksilver Student, the Bank of America® Customized Cash Rewards for Students, and many others charge zero annual fee.

Choosing a no-annual-fee student credit card is a no-brainer because you can afford to keep it in use forever and when you can use it for years, it is likely to impact your credit score positively as well. Remember, the credit history duration is a key factor for the FICO score.

2. Annual Percentage Rate (APR)

While keeping outstanding amounts and paying interest rates or APR against it is always advised against by the financial experts, you still need to opt for cards with a low student credit card APR rate just because in periods of financial troubles it cannot create a burden.

As per the report published by WalletHub on the latest credit cards, the average APR on credit cards for students with no credit is around 19.04%, while the APR for general credit cards averages around 22.11%. Financial institutions prefer to maintain this low APR for student credit cards as they consider students as the audience offering long-term opportunities.

You can even opt for a below-average APR rate and choose a 0% intro APR student credit card offer. There are several options out there that from time to time allows the cardholders to buy certain items with zero interest. Consider opting for a card with a 0% interest window in the initial years. This allows you to repay the amount without the interest piling up.

3. Credit Bureau Reporting

You may be surprised seeing this consideration in the list, but this can be key to improving your credit score and boosting credit eligibility in the long run. Many credit cards automatically do not send reports on your payment activities to all 3 principal credit bureaus such as, Equifax, Experian, and TransUnion. In that case, your credit profile is losing vital scores, at least, partially.

If you are serious enough to build a credit score as a student, you must make sure that all on-time payments are taken into account across all credit bureaus. So, when applying for any student credit card, always check whether it sends credit and repayment reports to all 3 credit bureaus or not.

4. Apply for Credit Cards that You are Eligible for

You can always be lured by credit cards that are not particularly meant for students and offer a much greater credit limit but you may find their approval criteria quite steep. Remember, applying for and getting rejected for cards that you are not eligible for, can actually make a negative impact on your credit score. This is why knowing the eligibility criteria before applying is so important.

The good news is that, the vast majority of student credit cards with no credit history requirements can be easily applied for. Some issuing companies like Discover and Capital One specialize in credit cards for students who have no credit score to show or have never had a credit card.

5. Rewards That Actually Match How You Spend

Any student credit card comparison list gives extra weight to this point. While reward is always a major attraction for students, considering the reward figures in isolation can completely go wrong for students. You need to put the rewards in the context of how college students spend money in their day-to-day lives.

A report published in the name of College Finance study, shows that online shopping happens to be the most popular credit card spending category for students with 70.1% spending rate followed by expenses on dining at 50%, and gas station spending at 44.4%. Naturally, any student credit card that offers you a 5% cash back on travel or 3x points on hotel accommodations, may not be that useful compared to cards offering reward points on online shopping, restaurants, and fuel purchases.

Some popular student cards optimize their reward programs for student spending patterns. For example, Discover it® 5% cash back on spending categories that rotate in every quarter covering restaurants, gas stations, and Amazon shopping. The Bank of America® Customized Cash Rewards for Students allows students to choose their preferred spending category for the highest reward points.

Last but not least, student credit card cash back rewards often become too complicated with layers and exclusions. It’s advisable to opt for a card that helps you save the most from your preferred spending categories.

6. Credit Limit and How It Increases

The vast majority of student cards come up with a basic credit limit, that goes anywhere between $300 to $1,500. While this is common to most cards, instead of this starting limit, you should look for cards that provide a clear and transparent step-by-step process to increase this credit limit.

This is important not just from the perspective of available spending amounts. A low credit limit can actually impact your credit score negatively. According to the FICO score guidelines, a higher credit utilization ratio is always damaging for credit score. With a higher credit limit, this utilization ratio is reduced resulting in a better score. Remember, the credit utilization ratio impacts the score irrespective of your timely repayment.

7. Look for Some Extra Perks

Apart from all the key considerations that we have discussed so far, you can look for some extra features that can add value to your experience. Below we picked a few of the,.

- Free credit score access: Can you check your credit score from time to time as a cardholder? Yes, this is important to stay focused on using the card to build a credit score. Several best student credit cards in the USA these days allow you to track your credit score every month for free.

- Reward against your GPA score: Yes, some cards reward you with free money if you score a higher GPA as per the bank. For example, Discover offers its student credit card holders a one-time $20 statement credit in every school year, provided you report a GPA score of 3.0 or higher.

- No foreign transaction fee: In case you are likely to apply to foreign universities or study abroad in the future, opting for a student credit card with zero foreign transaction fee can be a smart move. Foreign transaction fees go between 2 to 3% for every purchase, and the cost can add up very quickly.

- Purchase protection and extended warranty: There are also credit cards that offer additional protection through a warranty for selected purchases and this can be very useful for high-value purchases like electronics.

8. Consider a smooth upgrade option

What happens when your college days are over and you have become a young professional? You still may not use the same student credit card for college students and you need to upgrade to another card. Does the issuing bank or organization have a series of card products and does it allow previous cardholders to upgrade to a new card seamlessly? This is a crucial consideration.

If you are allowed to switch to a new card with the same account, you are saved from the labor of a new application and your credit history from the previous card continues uninterrupted.

The Bottom Line

So, if you set your priorities right and know the checklist by heart, picking the perfect student credit card in the US will not be difficult. Don’t weigh heavily on a single lucrative plus point; instead, make an all-round research covering all the key considerations and find the card that suits your spending patterns, credit score building, and future financial needs.

Author

Related News